Affordability Matters: The data from Water Matters 2024

Water Matters report – what are the findings telling us?

It has been a few months since CCW published Water Matters 2024 back in May. As the longest-running in-depth survey of water customers’ views, this research gathers a lot of detail. That’s why we have been following up with a series of shorter, ‘mini reports’ looking in greater depth at specific themes from the data.

This summary looks specifically at customer bills and affordability – a key issue, especially in the context of an ongoing cost-of-living crisis and the prospect of rising water bills from April 2025.

One of the stand-out findings from the previous year’s survey was the sharp rise – 53%, up from 34% – in the proportion of customers saying that their household financial situation had become either ‘slightly’ or ‘significantly worse’ in the last twelve months. Whilst we have seen a slight improvement on that figure this year – 48% said that their financial situation had got worse over the last year – this still shows that many people are worried about their circumstances. With this in mind, customer views on affordability of water bills are more important than ever.

Headline findings

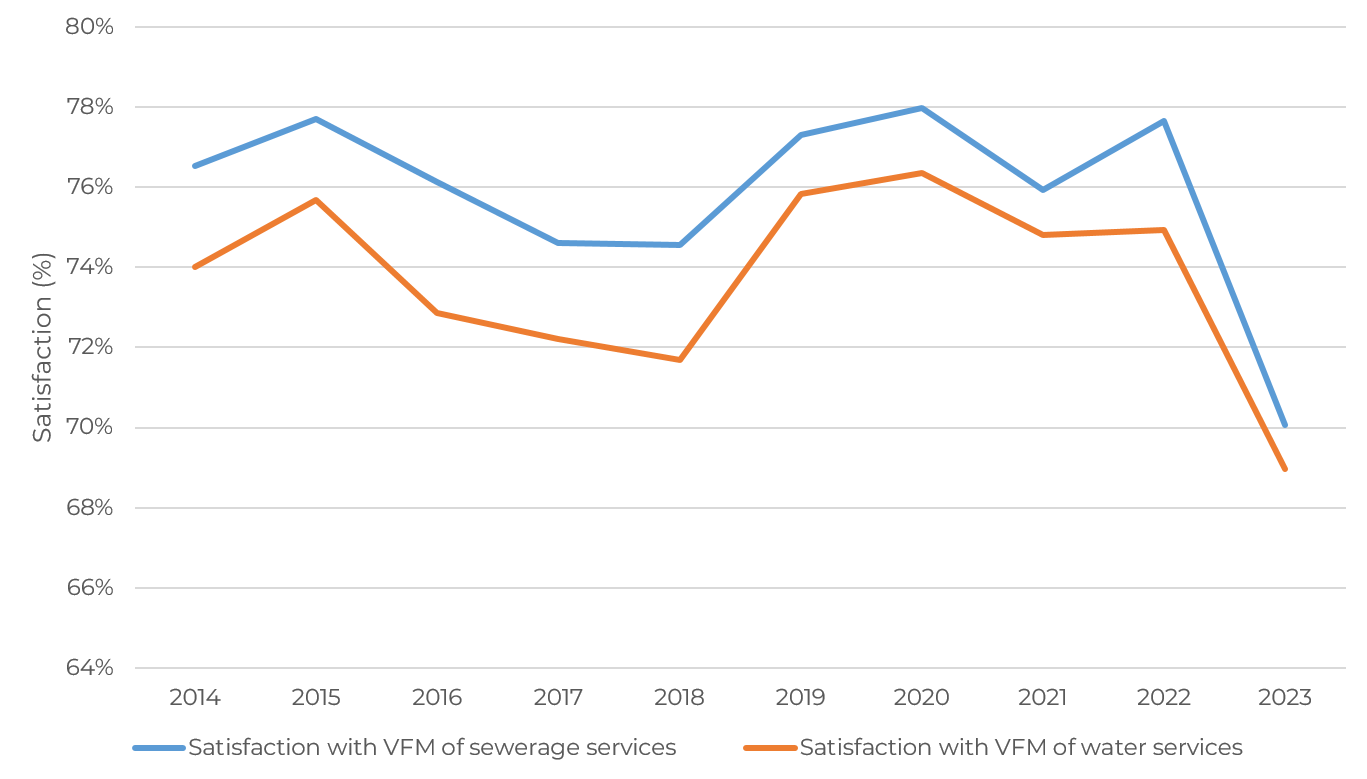

- This year saw the lowest recorded score for satisfaction with value for money of water and sewerage services – 69% and 70% respectively.

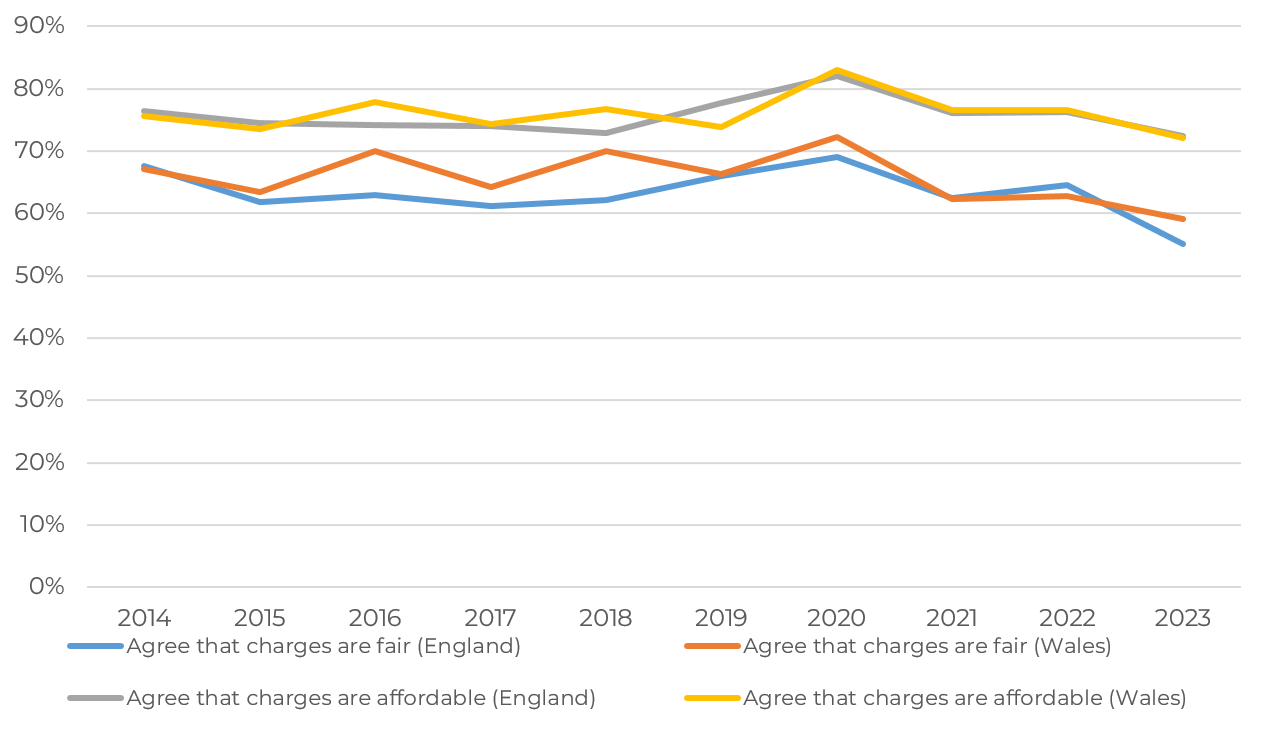

- The number of customers who find their charges affordable is 72% (down from 76%), which is 17% higher than those who find their charges fair, at 55% (down from 64%).

- Awareness of the various forms of financial support offered by water customers has continued to increase: there was a significant leap from 37% last year to 45% of customers who were aware that their company offered reduced bills to households that were struggling financially.

Last year’s Water Matters results were broadly positive when it came to value for money: while satisfaction with affordability of water services remained stable, satisfaction with affordability of sewerage services rose to its joint highest level.

This year, however, satisfaction with both plummeted to their lowest ever levels across England and Wales, in both cases recording the largest ever fall in year-on-year scores. (See Figure 1).

Across England, satisfaction with value for money with water services fell from 75% last year down to 69% – the first time this has fallen below 70%. Satisfaction in Wales was slightly higher (71%), but saw an even larger fall in a single year – down from 81% in 2023.

Despite the significant falls in satisfaction more generally with sewerage services that we saw throughout this year’s Water Matters, satisfaction with value for money of sewerage services was marginally higher than for water services (70%, compared with 69%).

Scores relating to value for money of both water and sewerage services were fairly uniform across different demographic breakdowns such as age, ethnicity and socio-economic group. Unsurprisingly, there were more significant variations in score when it came to different companies, reflecting the differing bill levels across England and Wales. For water services value for money, this ranged from 60% (South West Water) to 76% (Anglian Water); for sewerage services, this ranged even more significantly, from 52% (Southern Water) to 78% (Anglian Water).

One of the stand-out findings from the previous year’s survey was the sharp rise – 53%, up from 34% – in the proportion of customers saying that their household financial situation had become either ‘slightly’ or ‘significantly worse’ in the last twelve months. From that low bar, this year’s results gave little grounds for renewed confidence – there was a slight improvement on this metric, but 48% still said their situation had got worse.

Unsurprisingly, then, the proportion of customers who agreed that their bill was affordable dropped from 76% to 72%. However, there was a significantly larger decline in those who thought their bill was fair, down to 55% from 64%.

In every year of Water Matters results, people have been more likely to think their water bill is affordable than it is fair, with the difference between the overall averages being between 8% and 13%. This year, however, the gap has reached its widest ever level of 17%. One possible explanation for this drop in agreement around fairness of bills is that the collapse in trust, which we have been seeing over the past year, has filtered into a stronger feeling around the fairness (or unfairness) of bills. Certainly customers of the companies with low trust scores, such as Southern Water, Thames Water and South West Water, were also among the least likely to agree their charges were fair.

One of the more positive aspects of this year’s Water Matters findings is that awareness of the various financial support schemes in place by companies has risen to an all-time high.

Awareness of the social tariffs, whereby water companies offer reduced bills to households struggling with their financial situation, was up to 45% in England and 44% in Wales, compared to 37% and 41%, respectively, last year.

This increased awareness of financial support is encouraging, but there is still much further to go. As we explored in our previous Water Matters mini-report on customer service, fewer than half of customers (47%) in England and Wales think that their company communicates well on the availability of additional services specifically. This means that there is scope to improve communication, and so increase wider awareness of available support. This is an area we will continue to focus on in our work with companies, particularly sharing good practice so that the industry as a whole can do more to raise awareness.

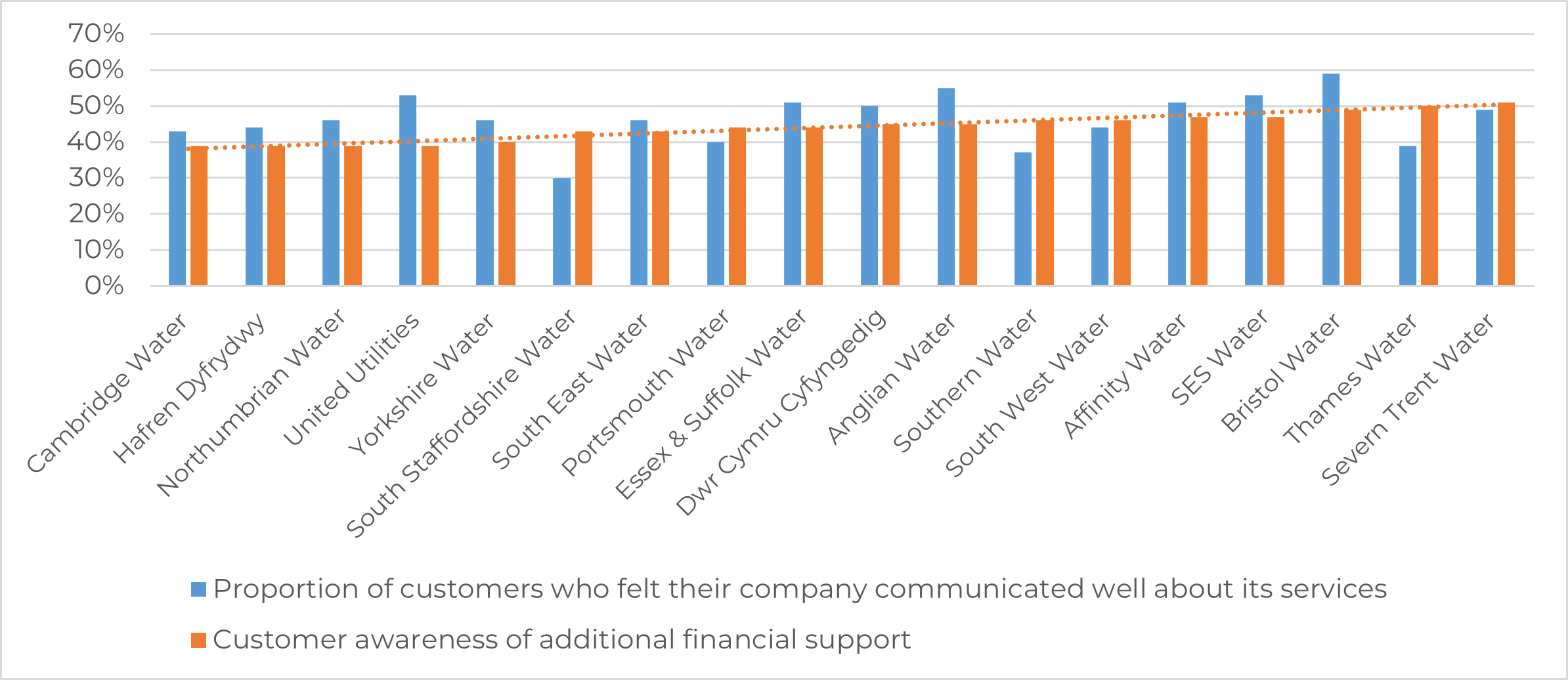

As Figure 3, below, shows, customer awareness of additional financial support varies by company: customers had noticeably higher awareness for companies which were felt to communicate well about the services they offered.

Conclusion

Our analysis of this year’s Water Matters report has highlighted that few customers think their financial situation is likely to improve in the near future, and the proportion who agreed that their bill was affordable has continued to fall.

Additionally, against the background of rising bills, customers are less inclined than ever to think they are receiving value for money from their water and sewerage services.

Support is available for customers that are struggling to pay their bills – and it is positive to see that more people are aware that this help is available. Our analysis shows that there is also a need for companies to consider how they can address and turn around the decline in people’s perceptions about the fairness of their bills. A step towards this could be clearer information on what people’s money is being spent on.

With trust in companies being at an all-time low, it is more important than ever to reassure customers that their money is being well-spent. As CCW’s recent research into customer-centric culture has shown, this kind of transparency is pivotal to rebuilding customers’ trust in water companies.